Long-Term Capital Management: Nobel Prize-Winning Math Needs $3.6B Bailout After Miscalculating Human Panic

What happened

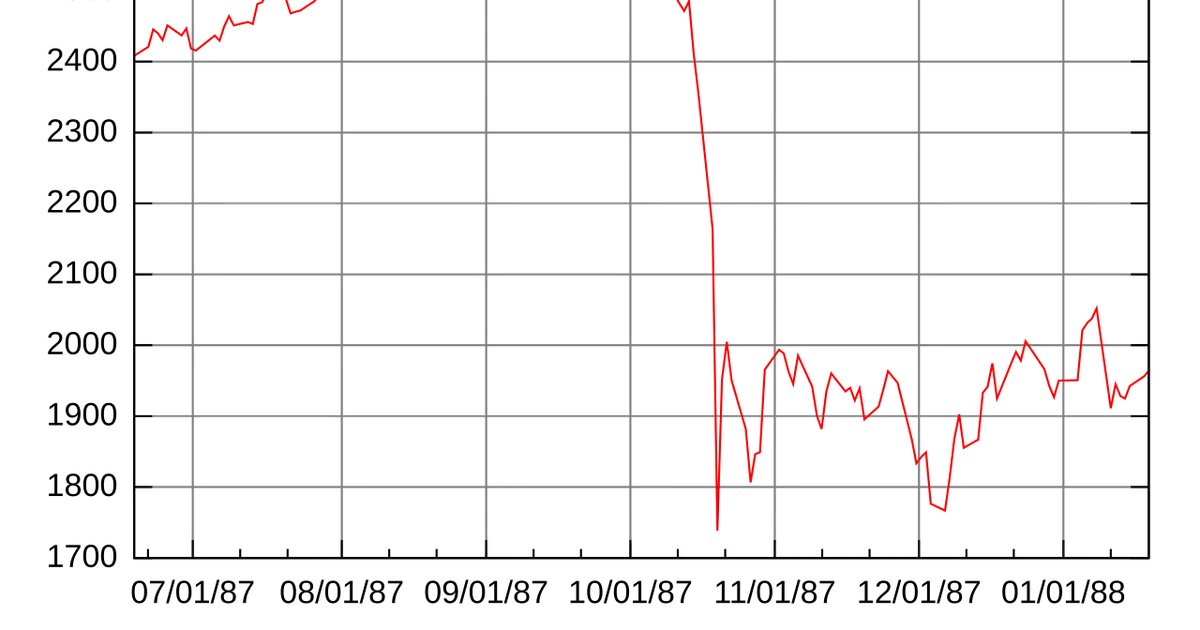

Long-Term Capital Management (LTCM), a hedge fund co-founded by Nobel Prize economists Myron Scholes and Robert Merton, nearly collapsed the global financial system in 1998. LTCM's models — which had delivered 40%+ annual returns for three years — failed catastrophically when the Russian financial crisis drove markets to move in ways the models deemed statistically impossible. The fund lost $4.6 billion in four months. The Federal Reserve organised an emergency $3.6 billion bailout by 14 major banks to prevent a wider collapse.[1]

What went wrong

LTCM's models were calibrated on historical data and assumed that the correlations between assets would remain stable. The models did not account for liquidity risk — the impossibility of unwinding enormous positions in a panicking market where everyone else is also trying to sell. Leverage of approximately 25:1 on equity and far higher on bond positions meant small moves against the book were existential. When the Russian default triggered a global flight to safety, assets that LTCM's models considered uncorrelated moved together. The fund was too large to unwind quietly; attempts to do so would have crashed the positions they were trying to exit.[1]

Lesson learned

A model built on historical correlations fails precisely at the moment it is most needed: when a novel shock causes everything to correlate that was previously independent. LTCM's Nobel Prize-winning mathematics was internally consistent — it simply excluded the scenarios that would break it. Financial risk models that don't include the distribution tails where all correlations go to 1 are not risk models at all.

Sources

- [1]

External links can go dark — pages move, paywalls appear, domains expire. Every source above includes a Wayback Machine snapshot link as a fallback. All citations are best-effort research; if a source contradicts our summary, the primary source takes precedence.